As of end of 2017, each household in Rwanda owed close to US$1,700[1] according to the amount contracted by the government with creditors on international and local markets. This amount is forecasted to increase as Rwanda will inevitably be borrowing throughout the coming years. An estimated US$ 1,250 of Rwanda government debt per household was owed in foreign currency while the remaining US$ 450 was owed in local currency in 2017. Although the local currency denominated debts are lower than those in foreign currencies, they are severely toxic to Rwanda’s economy. These debts consist of treasury bills and bonds issued by the government of Rwanda on the local bond market since 2012.

The first article of this series can be read from here.

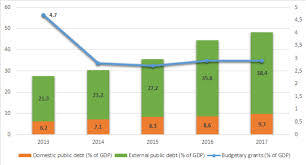

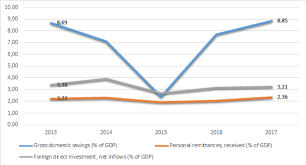

Advanced arguments in favor of launching a local bond market in Rwanda are yet to materialize. Rwandan Senior staff at the Ministry of Finance and Economic Planning, National Bank of Rwanda, and the Capital Market Authority argued that the development of a bond market in Rwanda will, among other, facilitate financial intermediation and domestic savings mobilization. They also argued it would reduce the country’s dependence on aid and foreign currency denominated borrowings (pg. 22). The reality, however, is that financial intermediation has somewhat expanded well before the introduction of a local bond market in Rwanda (pg. 45). Considering persistent low turnover of Rwanda’s bond market, its role in accelerating further financial deepening in Rwanda is yet to be determined. Moreover, while aid flow to Rwanda is reducing since early 2010’s, foreign currency denominated debts, that the local bond market was supposedly to reduce, have soared and so were domestic debts (See graph 1). Gross domestic and foreign savings such as remittance and foreign direct investment inflows have also remained unchanged over a significant period of time (See graph 2).

Graph 1

Data source: World Bank

As aid decline both Rwanda’s domestic and foreign debts has been increasing.

Graph 2

Data source: World Bank

Rwanda’s domestic and foreign savings levels have remained unchanged for the past 5 years.

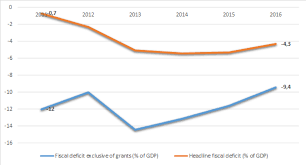

The evident motive to develop a local bond market in Rwanda is to finance the country’s persistent fiscal deficit. Rwanda’s headline fiscal deficit has widened from 0,7% of GDP in 2011 to -4.3% of GDP in 2016 as external grants reduce. The fiscal deficit, exclusive of grants, has dropped from -12% of GDP to -9.4% over the same period (see graph 3).The World Bank interprets these trends as an indication that Rwanda has been unable to maintain its spending amidst aid decline (pg. 11). Subsequently, the country’s government has been regularly borrowing from the local bond market to finance its budget deficit for development projects. The repercussions were that Rwanda’s domestic debt has almost tripled from $300 million (5% of GDP) in 2010 to $850 million (10% of GDP) in 2017. Though the Rwandan government’s objectives of financing the budget deficit from domestic borrowings is well intentioned, there are concerns to be stressed.

Graph 3

Data source: World Bank

Rwanda’s headline fiscal deficit has widened whilst fiscal deficit, exclusive of grants, has dropped

Regular loss of public funds borrowed from the local market is a concern. According to the audit reports compiled and published by the Rwanda’s Office of the Auditor General, the country has been losing an estimated average of US$17.8 Million worth of public funds through irregular public spendingeach year from 2010 to 2017. That is a total of $125 Million and equivalent to close to 25% of the US$550 Million that the country borrowed from the local bond market between 2010 and 2017. It is important to note that the level of aforementioned public funds loss could turn out higher than reported. This is because the estimated amount does not include other public fund loss such as services or goods paid but not delivered, unused assets, delayed and abandoned contracts etc. Moreover, according to Open Budget Survey 2017, the information in the audit report published by Rwanda is barely substantial and definitely not extensive. Therefore, the contents of the audit report might not be comprehensive in revealing the country’s public spending losses.

Interest payments on domestic debt are rapidly rising and have dire consequences on Rwanda’s economy. Recent reports fromThe World Bank point out that though the stock of Rwanda’s domestic debts are much lower than external debts, interest payments on domestic debt accounted for almost half of total interest payments in 2016 because of higher interest (pg. 12). The International Monetary Fund noted that Rwanda’s interest payment on domestic debt will remarkably increase throughout upcoming years from US$30 Million in 2015/2016 to US$75 Million in 2019/20. External debt interest payment will rise relatively lower than domestic borrowings from US$35.7Million in 2015/2016 to US$ 52 Million in 2019/2020 (pg. 21). Additional borrowings from the local bond market will significantly cause interest payments on debts to rise. This will further deteriorate Rwanda’s fiscal space and undermine the country’s debt sustainability as well as decelerate its economy.

Indebtedness is already impending Rwanda’s economy and preventing the country from reaching a middle income status by 2020. A World Bank report on Rwanda states: “Sustaining a high rate of growth in long-term and transitioning into a higher income status requires both strong productivity growth in the sectors and allocation of resources from less productive to more productive sectors, process known as a structural transformation”(pg.16). The report also demonstrates that Rwanda’s economic growth has been decelerating since 2011. The bank explains that, proceeds from Rwanda’s indebtedness have been skewed towards sectors where economic activities have not fully peaked up such as housing, tourism and conference, and less toward sectors where productivity growth is potential high such as tradable and manufacturing (pg. 18). Under such circumstances, Rwanda cannot reach a higher income status. In January 2018, the IMF was reported to warn Rwanda that the country will not meet its ambition to transform into a middle income economy by 2035 unless it grows domestic revenue and stops dependence on debt. Not only does this imply that Rwanda will not categorically attain its objective to transform into middle income state as stipulated in its vision 2020 development program, but it also means the country might not reach the status yearned for by 2035 unless its tax revenue level is considerably increased.

The rise in Rwanda’s government issuance of domestic bond coincides with a decline in credit growth for local commercial banks. This is due to nonbank investors, especially large institutional investors, drawing down their bank deposits to invest in the government bonds which offer competitive interest rates (pg. 8). The repercussion is that the local commercial bank’s lending capacity to spur private investment has been reducing over time. The credit growth has moved from 30% in June 2012 to below 0% in June 2017 (ibid) and the private investment contribution to GDP has reduced from 11.4% in 20012 to 8.3% in 2014 (WDI, August 2018). These trends imply that borrowing from local markets might have gradually crowded out private investments in Rwanda, leaving capital investment, largely generated from external and domestic borrowings as well as aid, the prime mover of economic growth for the country.

However, Rwanda’s economic growth model is not sustainable as it is driven by government investment which is generated largely from borrowing at the time of declining aid. The World Bank Rwanda report of August 2017 reads: “As both domestic private savings and private investments are low and the government is the main force behind investments, there is only limited scope to further increase public investments under the current (Rwanda) growth model” In its following report on Rwanda dated December 2017, the Bank states: “ With external grants declining and borrowing space for expanding public investment now limited due to higher public and publicly guaranteed debt, that (Rwanda) economic model might have reached its limits”. Finally, in its note on Rwanda’s ratings of May 2018, Moody’s, a credit rating agency, points out: “A continued rise in government debt levels, without evidence of stronger government revenue to service that debt and/or stronger capacity of the economy to absorb shocks would likely prompt a downgrade.”

Stakeholders should further investigate whether Rwanda’s borrowing spree has not been expanding income inequalities and subsequently impending human development in the country over time. Considering that some of the borrowed proceeds, if not lost through irregular public spending, were allocated in less productive economics activities; the Rwandan economy has not been able to create employments to a large share of the country’s unskilled labor force. Thus, income for a mass of ordinary people at the bottom level of the socio-political hierarchy in Rwanda remains meagre and at the same time subjected to strict taxation rules imposed by the government to raise sufficient revenue to service the debts. Moreover, according to the United Nation Human Development (UNDP), Rwanda Gini coefficient, an indicator of income inequality, has been high at 50.4 from 2010 to 2017. In this same period, the country’s domestic debt has tripled. Finally, while inequalities in, namely, education and life expectancy have been reducing in Rwanda, loss in Rwanda’s human development index emanating from inequalities in income have been increasing from 2010 to 2015. This implies that inequalities in income, that might have been driven by indebtedness, have been impeding human development in Rwanda. To avoid any ambiguity, independent and credible studies are prerequisite to further ascertain whether Rwanda’s borrowing spree has not been expanding income inequalities in the country rather than prosperity.

Way forward:

Many Brentwood institutions’ reports on Rwanda comprise suggestions to make the country’s economy less dependent on debt. For instance, the IMF has been recommending Rwanda to increase its domestic revenue capacity while The World Bank suggests Rwanda to put efforts in developing a productive private sector. These proposals have proven to be difficult to accomplish for Rwanda, despite the country’s claims of having achieved high economic growth for decades. One particular area that Brentwood institutions are yet to recommend Rwanda to improve on is governance. In my view, Rwanda’s governance ought to be revamped to enable, among others, efficiency in deploying scarce resources, transparency in public management and fair citizen participation. In the absence of an organized and proactive political opposition, as well as an unbiased parliament capable of challenging the incumbent government on its management of finance raised from borrowing, Rwanda’s indebtedness will remain on raise in vain and, as such, becomes a hindrance to its citizens’ human development in the long run.

Aimé Muligo Sindayigaya

To read more articles written by the author visit http://insightfulquotient.com/